It has been an another amazing year for Bank Marketing Strategy in 2013. The blog was named a top financial industry blog for the second straight year by The Financial Brand and bank and credit union industry followers viewed articles more than 600,000 times during the year.

But which of my 72 posts in 2013 were the most popular? Based on readership, it looks like posts dealing with banking strategies, mobile banking, new competition, and distribution topped the list over the past twelve months. Readers also read my crowdsourcing posts in record number, where dozens of global industry leaders contributed their insights.

Below are this year's top 10 articles with links to each post.

Banking Leaders Predict Major 2013 Trends

Not surprisingly, the most read post during the past year was also one of the first posts of the year, where more than 50 financial industry leaders provided their insights and predictions for what they believed would occur during 2013.

Predictions included thoughts on payments, big data, delivery channels, marketing technology, product and segmentation opportunities, competition and compliance. Many of the contributions were spot on, while some were ahead of their time.

Interestingly, the 2014 Top 10 Retail Banking Trends and Prediction post published last week also is also a top 10 article for 2013.

Moven: From Mobile Banking to Mobile Money

Curiosity about new financial industry players like Moven, Simple, GoBank and new product introductions like Bluebird from American Express continued to generate a large number of readers in 2013.

While these mobile-first banks may have been ahead of their times a couple years ago, much of their vision of simplicity, an improved user experience and integrated personal financial management tools are quickly becoming table stakes in the battle for the mobile banking customer. This post illustrated how Moven continues to be one of the leaders in being able to leverage the power of the smartphone as a payment device with the ability to provide immediate feedback with every spending decision.

Banking Leaders Discuss 2014 Strategic Planning Priorities

To assist with bank and credit union strategic planning processes, I enlisted the help of more than 30 banking leaders from across the globe in July to provide thoughts on the priorities that should be considered in the upcoming year.

Despite responses coming from disparate locals, the recommendations were surprisingly consistent, with a focus on enhancing the customer experience, better defining mobile positioning, integrating delivery channels, reducing enterprise costs, leveraging data, improving sales and marketing effectiveness, defining a differentiation strategy and continuing to focus on revenue, security and compliance.

9 Ways Marketing Can Help Acquire New Mobile Banking Customers

Many bank and credit union executives realized that just because you build a mobile banking application doesn't mean customers will automatically enroll for and use mobile banking . . . especially beyond balance inquiries.

This post discussed how marketing can greatly improve the adoption rate of mobile banking by actively marketing the service using all of the communication channels available.

From ATM receipts to online banking banners and social media, this post provided real world examples of how banks across the country are promoting the mobile banking channel.

Top 10 Retail Banking Trends and Predictions for 2014

Despite only being published 15 days before the end of the year, this crowdsourcing post quickly became one of the most read posts of 2013 by followers of the bank and credit union industries.

Sharing the insights of more than 60 bankers, credit union executives, financial industry analysts, bloggers and advisors, this post provides the foundation for both planning and implementing plans in 2014.

From the overarching 'drive-to-digital' and disruption of the payments world to the breaking down of internal silos and rethinking delivery networks, there will be extensive change in the coming year.

Building a Winning Mobile Banking Strategy

No area of banking was more active than the development and improvement of the mobile channel in 2013. That is probably the primary reason this post on how to develop a mobile banking strategy was so popular.

This post included a discussion of some of the great work Forrester Research has done in the development of a Mobile Banking Strategy Playbook and referenced their Global Mobile Banking Functionality Rankings as a foundation for looking at what some of the best in the industry are doing.

This post also complimented a later 'best in mobile' post entitled, My Digital Banking Nirvana.

From Passbook to Mobile: The Evolution of the Bank Account

Of the many excellent guest posts done for Bank Marketing Strategy, the discussion of the evolution of the traditional bank account by Brett King was the most read during 2013.

Reinforcing the underlying theme of his best selling book, Bank 3.0, this post set the stage for the many changes that occurred in the mobile banking space in 2013 including the introduction of King's mobile-first bank, Moven.

While we may not see a branchless future for some time, it's clear we're headed for a less branch future.

5 Bank Marketing Strategy 'Quick Wins'

Another very highly read post from January of 2013 was a post that discussed some of the can't-miss strategies I have seen work across the country at banks and credit unions of all sizes. Possibly airing some of my frustrations around why organizations expend energy on difficult and risky initiatives when much easier and financially beneficial strategies get little attention, this post provided ideas that could get the year started on a positive note.

Keys to winning through new mover acquisition, digital retargeting, new customer onboarding, cross-selling using triggers and the collection of insight for improved customer communication were all highly suggested as a way to increase revenues and reduce costs.

Will The Power of Mobile Make Bank Branches Disappear?

There was a lot of discussion throughout 2013 as to whether the mobile channel will replace traditional branches in the foreseeable future. This February post dug into a Bain & Company report that found that a strong mobile banking application could improve the likelihood of a positive customer referral of the bank or credit union.

The research also found that customers that used mobile banking were less likely to go to a traditional branch as often and that development of 'premium' mobile banking apps have a positive impact on the acquisition and retention of mass affluent and affluent customers.

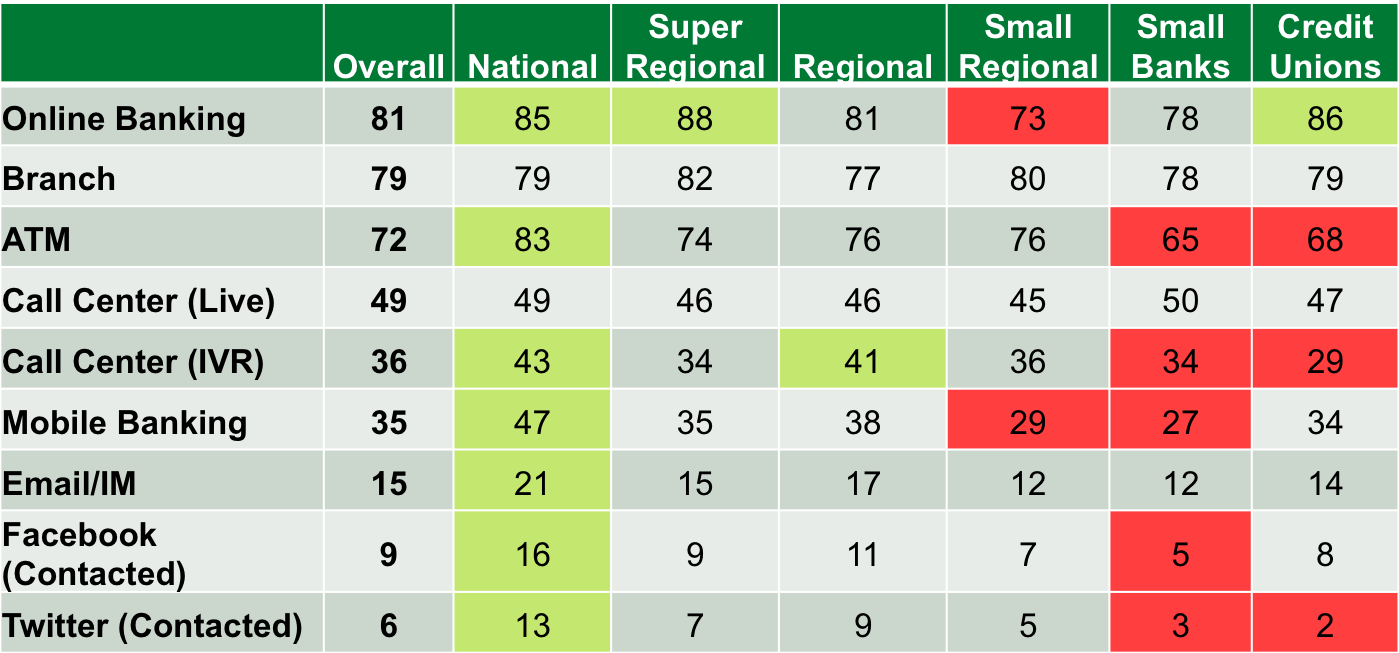

Migrating Customers to Digital Channels

While terminology like 'omnichannel' became part of our industry's lexicon in 2013, and the desire to migrate customers to digital channels was on top of most financial organization's to-do list, there was evidence that customers have different channels they prefer for different activities.

This May post used Gallup research to illustrate that most customers don't want to use just one channel and that 'forcing' a customer to use a channel they didn't prefer impacted both satisfaction and engagement.

Providing details into channel preferences by banking activity (making deposits, paying a bill, etc.), this post provided some eye opening insight into the risk of 'channel mismatches.

Demographics No Longer Effective For Financial Direct Marketing

Over the past several weeks this post and the preceding post kept switching positions as the number ten post, so I thought I would include both in this year's rankings due to the importance to financial marketers.

Referencing insight from numerous research studies, this post made it clear that relying on traditional age, income, occupation and education parameters is no longer enough. Instead, the post shows the power of advanced segmentation that leverages behavioral insight like channel use, product ownership, transaction levels and types, etc. While many bank and credit union marketers are already using these expanded sources, others continue to use only standard demographics with limited success.

A lot of changes occurred in the financial services industry in 2013, and it appears that the disruption will continue in 2014. I hope my blog brings some clarity to what is happening in our industry and that I can continue to be a resource that you can rely on going forward.

I am humbled by the number of readers I had in 2013 and am committed to sharing insight and observations I have as I travel and visit organizations globally.

Happy New Year!

A lot of changes occurred in the financial services industry in 2013, and it appears that the disruption will continue in 2014. I hope my blog brings some clarity to what is happening in our industry and that I can continue to be a resource that you can rely on going forward.

I am humbled by the number of readers I had in 2013 and am committed to sharing insight and observations I have as I travel and visit organizations globally.

Happy New Year!